Trump’s New Trade War Tool Might Just Be Antique China Debt

Collectors of pre-Communist debt are lobbying the White House to force Beijing to make good.

By

Tracy Alloway

President Donald Trump’s next move in an increasingly fraught trade

war with China could be one for the history books, literally. The Trump

administration has been studying the unlikely prospect of reviving

century-old claims on Chinese bonds sold before the founding of the

communist People’s Republic.

The defaulted China bonds can be found in the attics and basements of thousands of Americans, or on EBay, where the certificates sell as collectibles

for as little as a few hundred dollars each. The PRC, which succeeded

the Republic of China after it replaced the imperial dynasty, has never

recognized the debt, though that hasn’t stopped decades of attempts to

collect payment on it.

Now, with Trump ratcheting up the trade rhetoric

with China, holders of the antiquarian bonds are hoping he’ll press

their case, even as other parts of the U.S. government are accusing

people of fraudulently selling the same paper.

Perhaps the only thing more peculiar than the story of the

Chinese debt and the bid to seek payment on it, is the cast of

characters drawn into its orbit. President Trump, U.S. Treasury

Secretary Steven Mnuchin, and U.S. Commerce Secretary Wilbur Ross have

met with bondholders and their representatives. Kirbyjon Caldwell,

pastor of a Texas megachurch and spiritual adviser to George W. Bush,

has been charged by the U.S securities regulator for selling the debt to

elderly retirees. (Caldwell has pleaded innocent and maintains that the

bonds are legitimate.)

“With

President Trump, it’s a whole new ballgame,” says Jonna Bianco, a

Tennessee cattle rancher who leads a group representing

pre-revolutionary China bondholders and who has met with the president.

“He’s an ‘America First' person. God bless him.”

Hundreds,

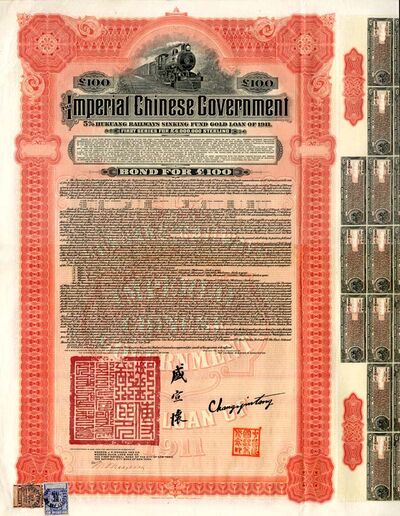

if not thousands, of these 5% Hukuang Railways Sinking Fund Gold Loan

of 1911 bonds—issued in 1911 by a consortium of banks in London, Berlin,

Paris, and New York—appear to have survived.

The

Hukuang Railway bond is a thing of beauty. Printed with an ornate

border and carrying a large chop, the debt was sold in 1911 to help fund

construction of a rail line stretching from Hankou to Szechuan.

The U.S. once referred to the money that flowed into China at

the turn of the 20th century as “dollar diplomacy”—a way of building

relations with the country (and its massive untapped market) by helping

it industrialize. The Chinese have another term for it: For them it fits

squarely into China’s “Hundred Years of Humiliation,” when the Middle

Kingdom was forced to agree to unfair foreign control.

Soon after

the imperial dynasty was overthrown in 1911, the Republic of China

began tapping the international capital markets for funding too. That

included selling a series of gold-backed notes to fund the nascent

country. It’s these bonds that Bianco, who co-founded the American

Bondholders Foundation in 2001 to represent holders of pre-communist

debt, is hoping could be a useful political leverage in Trump’s fight

with China.

“The People’s Republic of China dismisses its defaulted

sovereign obligations as pre-1949 Republic of China debt, but doing so

contradicts the PRC’s claim that it is sole successor to the ROC’s

sovereign rights,” Bianco said in an emailed statement in response to

this story.

Bianco says she’s spent years researching the issue

and recruiting high-profile proponents to the ABF team, including Bill

Bennett, who was U.S. Secretary of Education under Ronald Reagan; Brian

Kennedy, senior fellow at the Claremont Institute; and Michael Socarras,

Bush’s nominee for Air Force general counsel.

She argues that

China is in selective default, having paid out on bonds held by British

investors in 1987 as part of the Hong Kong handover deal negotiated by

former Prime Minister and ‘Irony Lady’ Margaret Thatcher. If China

doesn’t pay out, she says, it should be blocked from selling new debt in

international markets. By Bianco’s reckoning, China now owes more than

$1 trillion on the defaulted debt, once adjusted for inflation,

interest, and other damages—a sum roughly equivalent to China’s holdings

of U.S. Treasuries.

“What’s wrong with paying China with their own paper?” says Bianco.

From

left: President Trump, Jonna Bianco, and Brian Kennedy on Aug. 12,

2018, at the Trump National Golf Club in Bedminster, N.J.

Source: Jonna Bianco

She

met with Trump at his sprawling golf course in Bedminister, N.J., last

August, in an encounter she describes as “wonderful.” Since then she’s

met with Mnuchin, though she won’t reveal what was discussed. ABF reps,

including Bennett, Kennedy, and Socarras, met with Commerce Secretary

Ross in April, Bianco says.

People familiar with the Treasury

Department say the China bonds have been studied, but ABF’s

suggestions—including the possibility of selling the defaulted debt to

the U.S. government to then exchange with China—aren’t legally viable.

Spokespeople for Treasury and Commerce declined to comment. People

familiar with the views of Chinese officials say they’re aware of the

meetings, but they don’t think the claims can be revived.

At issue is a statute of limitations that has long run its

course and the fuzzy legal obligations of governments that inherit their

predecessor’s debts following civil upheavals. In one of the most

famous cases, the Soviet Union repudiated bonds sold under the Tsar,

inflicting losses on thousands of investors who had snapped up the

paper. Still, most agree that as a legal principle, political regimes

inherit their predecessors’ debt; most governments choose to honor old

bonds, in part because they don’t want to alienate investors who might

buy new ones.

“I think everyone who works for Trump at the

Treasury Department thinks this is loony,” says Mitu Gulati, law

professor at Duke University and a sovereign-debt restructuring expert.

“But I can’t help but be tickled pink, because at a legal level these

are perfectly valid debts. However, you’ve got to get a really clever

lawyer to activate them.”

Clever lawyers have tried before. The closest anyone got to

wringing payment out of China was a class action suit brought by holders

of Hukuang railway bonds in 1979 that managed to bring the PRC to court

to defend itself for the first time. Gene Theroux, formerly senior

counsel at Baker & McKenzie LLP, helped represent the Chinese

government in court.

Theroux, now retired, remembers the landmark

case well. “The requests of us as lawyers were occasionally unusual,” he

says, including China nixing any citation of previous cases with

“Republic of China” in the title, given its refusal to recognize the

regime under its “One China” policy. (Eventually, Baker & McKenzie

resolved the problem by citing old cases as “Republic of China

[so-called].”)

The suit was thrown out on the basis that the 1976

Foreign Sovereign Immunities Act, which allows U.S. courts to hear

cases against foreign governments for commercial claims, could not be

retroactively applied to bonds issued at the turn of the century.

Since then, a 2004 Supreme Court decision ruled that the FSIA could apply retroactively in a case immortalized in the movie Woman in Gold.

The ruling paved the way for Maria Altmann to reclaim paintings by the

famous Austrian artist Gustav Klimt decades after they’d been seized by

the Nazis.

That

still leaves the problem of reactivating modern legal claims on debt

that is now decades old. Gulati argues that this could perhaps be

done—for instance, by arguing that China making payments on modern bonds

violates pari passi (equal payment) clauses embedded in the

historic debt. Such clauses were successfully used by hedge funds

seeking payment from Argentina a few years ago. It’s a legal long shot,

but one that Gulati has assigned to his law students as a theoretical

exercise.

The U.S. Securities and Exchange Commission is studying

the debt, too. In a 2018 complaint against Pastor Caldwell and a

self-described financial planner named Gregory Alan Smith, the SEC accused the pair

of raising at least $3.4 million by persuading 29 investors to buy the

pre-revolutionary bonds. Some of the buyers, mostly elderly retirees,

liquidated their annuities to invest, the SEC said.

Messages left for Caldwell’s lawyer, Dan Cogdell, weren’t

returned. In a press conference in March, Cogdell said the charges

against his client were “false.” Caldwell, who was educated at Wharton

before working as a bond salesman at First Boston and going on to

officiate at Jenna Bush’s wedding, said the bonds are “legitimate” and

has returned money to investors at their request. Smith entered a plea

agreement to the charges last month.

“Defendants falsely

represented to these investors that the bonds were safe, risk-free,

worth tens, if not hundreds, of millions of dollars, and could be sold

to third parties,” the SEC said in its complaint. “In reality, the bonds

were mere collectible memorabilia with no investment value.”

—With Saleha Mosin, Jennifer Jacobs, and Steven Yang.

(Updates

with a U.K. bondholders agreement from 1987 in 11th paragraph .

Clarifies that ABF represents ROC bondholders in eighth paragraph,

includes response from ABF in ninth paragraph.)